OPEC has delivered real, impacting cuts but has communicated poorly to a bruised and low confidence paper market setup for a “beat”. This misread or (temporary) misappreciation of the crude oil picture as it stands, provides good risk/reward trading opportunities. There is a “Saudi Put”, which has big implications for traders to monetise mispriced option volatility structure and for hedgers to adjust hedges.

OPEC “RESULT”: Our base case last week (Scenario #3) was a bullseye read with the expected outcome of the 9-month extension to be a “…sell the news” event and the $51.46 bbl market close confirmed our forecast “…Market sells off Day1 to $51 – $52 bbl area …”.

Some market participants, emboldened by the use of “whatever it takes” by the Saudi Energy Minister, were positioned for a beat (we forecasted less than 20% probability of such an event according to our analysis).

The Saudi’s use of “a la central bank” language has created a Pavlovian-like response/expectation for post-2008 financial crisis traders. The difference is that western Central Banks have concocted the biggest ever alchemy of financial cocktail, whereas Thursday’s OPEC/NOPEC deal extension, in comparison, appears modest.

Still, OPEC is clearly not just talk and is delivering concrete, impacting cuts. They have delivered record beating compliance; and appear to have unanimously voted to extend cuts. It even looked like, for a brief moment, at least here from London, that Russia were a part of OPEC (and that says volumes to their concerted efforts).

The two most important oil ministers (Saudi and Russia) talked up the market as best as they could.

OPEC chose not to deepen cuts and to shift the curve in backwardation, but have committed to extend cuts, with talks of a further extension if need be. The market appears to have misread OPEC’s actions by focusing on the exit strategy (or lack thereof);

whereas the intention of OPEC’s communique was to highlight its commitment to balancing supply and demand and that barrels would not flood the market once the cuts ended.

The Saudis communicated this clearly, when they highlighted that the focus was going to be, not on production cuts only, but on export cuts. This again was missed as the market sentiment pendulum is currently opposite to what it was early in 1Q17.

More specifically, exports to the US are to be cut (under 7 mil bbl in May). Tanker tracking data and June loading programs support the reduced exports to the US. The champagne must have popped open in Houston on that comment during the press conference and perhaps is still flowing as this has direct consequences for WTI/sour crude spreads (and WTI/Brent).

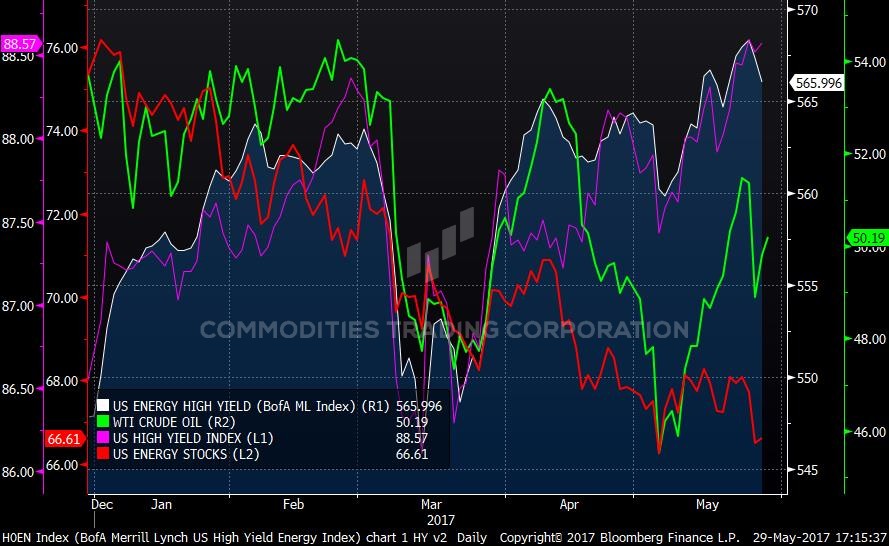

It was interesting watching our screens post the OPEC meeting. For example, why did WTI and US energy stocks sell off hard, whilst US high yield, and US energy high yield debt in particular, actually firmed? SEE CHART 1 –

Falling oil prices have a direct negative impact on equities – additionally producers cannot lock-in forward hedges. For energy debt, prices are far from levels that would indicate limits on credit availability despite ~$108 billion funding gap for tight oil producers. Actually, the conclusion of the OPEC meeting firmly solidified the view that oil prices should not fall significantly below shale’s marginal cost of production.

The trade then: Short the shares/ buy high yield as a result.

Chart 1 – US energy stocks, High yield & WTI – Daily YTD – Source: Bloomberg & CTC

PRICE ACTION & IMPLIED VOLATILITY: Let’s be clear, while our fundamental view of oil points to a much more constructive picture ahead, chart and momentum analysis point to greater uncertainty (at the very best).

Brent, as we write is trading just on Thursday’s close and below the 200-day moving-average (DMA) at $52.01 bbl. Current prices are well below the 100-DMA at $53.66 bbl and below Thursday’s important volume weighted average price (VWAP) of $52.85 bbl for Brent and $50.23 bbl in WTI are near term headwinds and clearly shorts are not “caught off-sides” here.

Note as well that our short, medium and long-term trading signals, replicating CTA/trend following funds, still point to “Sell” signals on all three.

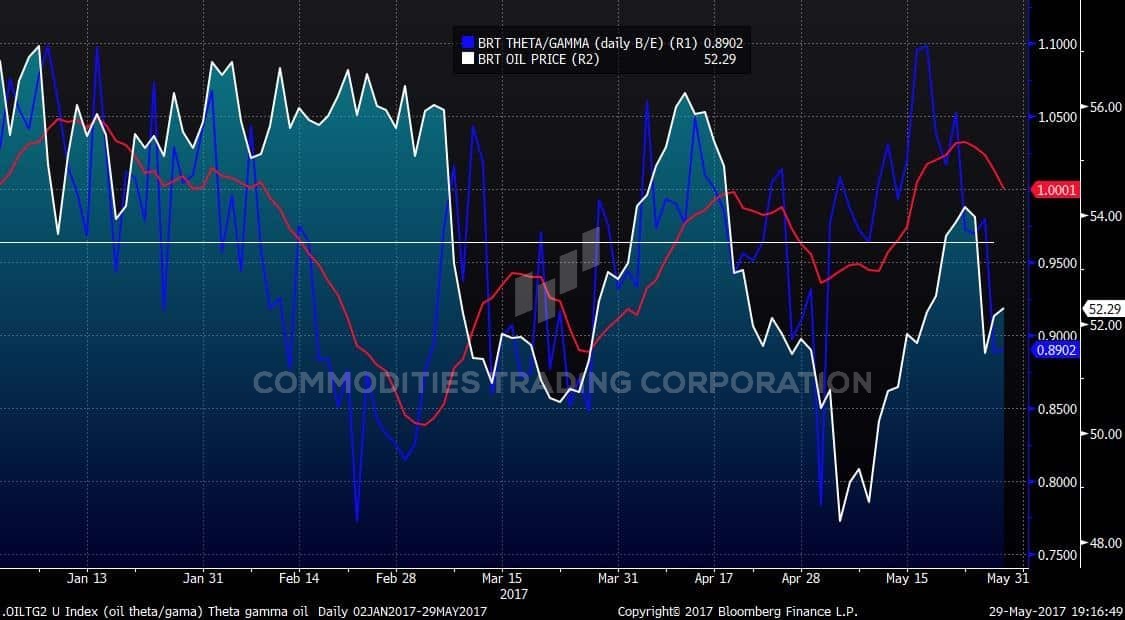

At first glance, it would be easy to point to short gamma positioning (increased volume in July

put activity in lead up to Thursday), but this does not hold up after further scrutiny.

First, front vol was only slightly up on the day, while flat price dropped over 5%. Second, on a daily $/bbl breakeven basis, vol was actually significantly lower – SEE CHART 2 – market makers would have bought gamma and not sold the underlying if that was the cause.

Analysis of open interest points to a modest change, given the flat price move: $500 million new shorts in WTI and $750 million length reduced in Brent. Certainly, the macro/ non-commodity centric funds who recently bought calls and calls spreads were pushed to take profit and sell.

The 4 – 5 vol put premium in DEC17 Brent, looks steep and unjustified, in our view a good opportunity to monetise – contact CTC trading desk for more on this.

Chart 2 – ICE Brent Price & Gamma (daily b/e) – Daily YTD – Source: Bloomberg & CTC

FUNDAMENTALS: The market is now shifting focus towards macro factors, oil demand (especially Asia), but more importantly, the market will need to see US stock draws in weeks ahead.

We see, OPEC cuts, especially to the US should provide a big psychological boost for confidence. The cuts should be reflected in the data and will be supportive for flat price with spreads to outperform.

We reiterate a summary of our views:

We see the “bull” confidence battered, just when physical draws in visible stocks are on the cusp of kicking in. There are a multitude of factors aligned for 2H17:

(1) OPEC/NOPEC: As it stands, the extended cuts highlights unanimous clear commitment (incl. Russia) from OPEC. If the 5yr average oil stock target has not been reached by the end of 1Q 2018, there is no reason to doubt and extension and a controlled exit strategy (as opposed to a flood) and all combined Asia exports cuts, redirected to the US.

(2) Non-OPEC: At this point, higher non-OPEC production (incl. US) has been factored in to the price. Nigeria (especially the return of Forcados) and Libya production have rebounded and production now, is more a market risk to disappoint, than to surprise to the upside.

(3) Demand: The bulk of refinery maintenance has happened. Globally, 5 million bpd of increased crude throughput are estimated to return from early May to end of June. This is constructive for crude oil demand and will weigh eventually for refinery margins.

(4) OPEC (and especially Saudi’s) crude domestic destocking done: OPEC’s exports to become more aligned with production cuts. Combined with the seasonal demand upswing – visible stock draws should accelerate.

(5) Floating storage (especially in Asia) will drawdown in 2H17: Global demand is not weakening but stabilising (US gasoline, India).

(6) Strong tailwind from derivative positioning: The total notional invested in crude oil is significantly below recent and 5yr averages. Flattening curve structure should attract pension portfolios rotating towards commodities as backwardation means investors are paid to hold the long position, even if oil does not perform.

Contact CTC to know about more about how we help with risk-management, hedging related services and trading views: contact@comtradingcorp.com.

Leave us a feedback

[contact-form-7 id=”3212″ title=”Feedback”]

Commodities Trading Corporation is a London-based private advisory company specialized in commodity risk-management and hedging. We service a growing need in the natural resources sector for unbiased and strong expertise and provide our services to an array of corporate clients and financial institutions. We are experts in derivatives and monetizing volatility and develop corporate strategies for hedging energy portfolios, using bespoke derivatives solutions for price risk mitigation.

For more information about what we do, how we can optimize your hedges and directly improve your bottom line, contact us at contact@comtradingcorp.com.

Authorised and Regulated by the Financial Conduct Authority (“FCA”).

CTC Marketing Commentary Disclaimer – This marketing communication has been prepared by CTC traders and sales personnel. The information contained within this marketing communication is general market commentary providing only the views an opinions of CTC traders and sales team. The views and opinions expressed herein may be changed at any time without notice. This material provides only a limited view of the market and does not constitute investment advice and or investment research. It has not been prepared with the legal requirements to promote the independence of investment research. It is also not subject to any prohibition on dealing ahead of the dissemination of any investment research. The information provided does not constitute an inducement, invitation or offer to engage in any investment activity. CTC neither makes nor gives any representation or warranty, express or implied as to the accuracy or completeness of the information and opinions contained and no responsibility or liability is accepted by CTC for the same and CTC shall not be liable for any direct, indirect or consequential loss or damage suffered or incurred by any person upon reliance of any statement or opinion or other such information. This communication is directed at CTC‘s professional customers and not intended for retail or private customers.